Debt Service Coverage Ratio Loan Explained: How to Get a DSCR Loan!

A DSCR loan, short for Debt Service Coverage Ratio loan, offers real estate investors an opportunity to secure financing for an investment property based on its rental income rather than their personal earnings.

These loans are particularly well-suited for self-employed investors, those managing multiple mortgaged rental properties, and individuals seeking to expedite the growth of their investment portfolios.

This page offers a comprehensive overview of DSCR loans with a clickable menu to skip to certain chapters.

Table of Contents

Chapter 1: What is a DSCR Loan?

DSCR loans are a type of financing arrangement commonly used in real estate investments.

These loans enable real estate investors to qualify for the purchase or refinance of investment properties primarily based on the rental income generated by those properties, rather than relying heavily on their personal income and creditworthiness.

The key feature of DSCR loans is the focus on the property’s ability to cover its own debt service obligations, which include the mortgage payments, property taxes, insurance, and any other associated costs.

Lenders calculate the Debt-Service Coverage Ratio (DSCR) by comparing the property’s Net Operating Income (NOI) to its Total Debt Service.

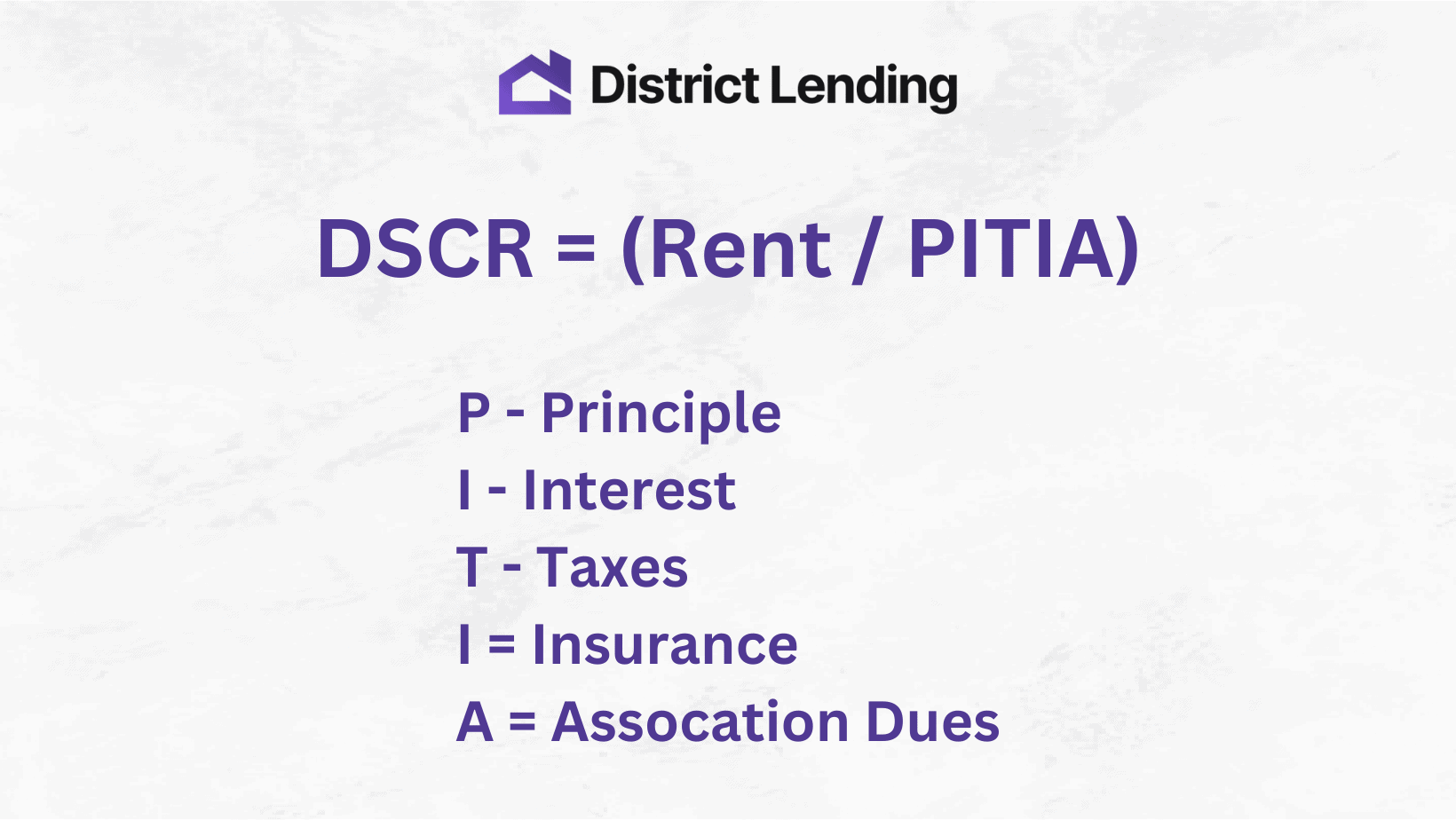

The DSCR ratio is a tool to help lenders understand a borrower’s ability to pay back a loan based on the monthly rental income of the property divided by the monthly principal and interest payments, taxes, insurance, and association dues (PITIA).

Calculating DSCR: The DSCR Equation With Examples

Here are some examples of how DSCR loans work in practice with examples:

DSCR = (Rent / PITIA)

PITIA = Principle, Interest, Taxes, Insurance, and Association Dues

For a commercial or multi-family property, DSCR is calculated by dividing the annual Net Operating Income (NOI) by the Annual Debt Service.

Note: The Annual Debt Service is the same as the annual PITIA.

What is the Formula for Commercial Property DSCR?

For example, if a property generates NOI of $60,000 annually and its annual debt service is $48,275, the equation is:

DSCR = ($60,000 / $48,275) = 1.24

The annual debt service in this example is less than the Net Operating Income, which makes the monthly cash flow positive.

What is a Good DSCR Ratio?

Generally, a “good” DSCR ratio is any number above 1.20.

Lenders typically look for a DSCR ratio above 1.20, means the property is cash flow positive at a healthy profit.

- If your DSCR is greater than 1.00, you are cash flow positive at a profit.

- If your DSCR is less than 1.00, you are cash flow negative at a loss.

- If your DSCR equals 1.00, you are cash flow neutral and break-even.

Chapter 2: What are the Pros and Cons of DSCR Loans?

Debt Service Coverage Ratio (DSCR) loans have both advantages and disadvantages, and whether they are suitable for you depends on your financial situation, investment goals, and risk tolerance.

Here are the Pros and Cons of DSCR loans:

DSCR Pros:

- Favorable Interest Rates: DSCR loans, especially those secured by real estate, often come with competitive interest rates compared to other forms of financing due to the collateral involved. Note, however, that DSCR loans tend to be higher than traditional consumer loans.

- Leverage: DSCR loans allow you to leverage your existing assets or income to invest in additional properties or expand your business, potentially increasing your overall wealth.

- Cash Flow Management: DSCR loans can help stabilize your cash flow by providing additional capital for property improvements, debt consolidation, or business expansion.

- Investment Opportunities: DSCR loans enable you to take advantage of attractive investment opportunities that may generate positive returns and enhance your portfolio.

- Tax Benefits: The interest paid on DSCR loans for certain investment properties may be tax-deductible, potentially reducing your overall tax liability.

- Long-Term Financing: DSCR loans often offer extended repayment terms, allowing for more extended investment horizons and lower monthly payments.

- Portfolio Diversification: Investors can diversify their holdings by acquiring different types of properties or assets using DSCR loans, spreading risk across various investments.

- Potential for Appreciation: Real estate investments financed with DSCR loans may benefit from property appreciation over time, potentially increasing the value of your assets.

DSCR Cons:

- Risk of Default: If your cash flow drops or your investments underperform, you may struggle to meet the DSCR requirements, increasing the risk of loan default and potential loss of collateral.

- Collateral Requirement: Many DSCR loans require collateral, such as real estate or business assets. If you cannot provide suitable collateral, securing the loan can be challenging.

- Stricter Qualifications: DSCR loans often have stricter eligibility criteria, including higher credit scores, more substantial financial documentation, and specific DSCR thresholds that borrowers must meet.

- Potential Loss of Assets: If you default on a DSCR loan, the lender may seize and sell the collateral to recover their investment, potentially leading to the loss of valuable assets.

- Interest Rate Risk: If your DSCR loan has a variable interest rate, you may be exposed to fluctuations in interest rates, leading to higher debt service costs over time.

- Limited Liquidity: DSCR loans tie up assets or income for the duration of the loan term, potentially limiting your liquidity for other investment opportunities or financial needs.

- Market Risk: Real estate investments funded through DSCR loans are subject to market fluctuations, and property values can decline, affecting the value of your collateral.

- Debt Burden: Taking on additional debt through DSCR loans can increase your overall debt burden and financial obligations, potentially making it harder to manage cash flow and meet other financial goals.

Chapter 3: What are the DSCR Loan Property Types?

The suitability of DSCR loans depends on the income-generating potential and risk associated with each property type.

Here are some property types that often qualify for DSCR loans:

DSCR Loans are generally suitable for the following types of properties:

- Airbnb Rentals: Yes, can you use a DSCR loan to buy Airbnb rental properties. DSCR loans are great for these types of investment properties because you can potentially generate income quicker due to faster closings. DSCR loans can be utilized to fund Airbnb properties, taking into consideration the prevailing rental rates for properties in the vicinity or Airbnb rates, especially if you possess a well-established hosting track record.

- Multifamily Properties: DSCR loans are frequently used for apartment buildings, duplexes, and other multifamily properties. These properties generate rental income from multiple units, making them well-suited for DSCR calculations.

- Commercial Properties: This category includes retail spaces, office buildings, warehouses, and industrial properties. DSCR loans are applicable when rental income from commercial tenants is the primary source of repayment.

- Vacation Rentals: Properties used for short-term vacation rentals can also qualify for DSCR loans if the rental income can consistently cover the property’s expenses and mortgage payments.

- Mixed-Use Properties: DSCR loans can be used for mixed-use developments that combine residential and commercial spaces, as long as the rental income adequately covers expenses.

- Single-Family Rentals: While less common, DSCR loans can be used for single-family rental homes, especially for real estate investors who own multiple single-family properties and seek financing based on rental income.

- Student Housing: Properties designed for student housing can also qualify for DSCR loans, provided that the rental income supports the loan’s debt service.

- Assisted Living Facilities: DSCR loans may apply to properties such as senior housing, assisted living facilities, and nursing homes, depending on the specific circumstances and income stability.

- Mobile Home Parks: Mobile home parks that generate rental income from tenants can be considered for DSCR loans.

DSCR Loans are generally not suitable for the following types of properties:

- Raw Land: DSCR loans are typically not used for financing undeveloped or raw land, as there is no rental income generated from such properties.

- Fix-and-Flip Properties: Properties intended for short-term renovation and resale, commonly known as fix-and-flip properties, may not be ideal candidates for DSCR loans. These projects typically rely on different financing arrangements, such as hard money loans or construction loans.

- Speculative Development: DSCR loans may not be suitable for speculative real estate development projects where income generation is uncertain or long-term.

- High-Risk Properties: Properties with a high level of risk or uncertainty, such as those in severely distressed neighborhoods or properties with significant environmental issues, may face challenges in securing DSCR loans.

- Vacation Homes for Personal Use: While some vacation rental properties may qualify for DSCR loans, vacation homes that are primarily for personal use and have limited rental income potential are not typically eligible for this type of financing.

- Non-Traditional Properties: Some unique or non-traditional properties, like historic buildings with high renovation costs, may not meet the criteria for DSCR loans due to the complexity of their financial structure.

Why Do Investors Like DSCR Loans?

DSCR (Debt-Service Coverage Ratio) loans hold significant importance for real estate investors for several reasons:

- Property Based Income Qualification: DSCR loans allow investors to qualify for financing primarily based on the income generated by the investment property itself, rather than relying heavily on their personal income or creditworthiness. This is particularly beneficial for investors who may have irregular or self-employment income.

- Portfolio Expansion: DSCR loans are instrumental for investors looking to grow their real estate portfolios rapidly. By using the rental income from existing properties to qualify for new loans, investors can acquire additional income-producing assets without being constrained by their personal finances.

- Risk Mitigation: Investors can reduce their personal financial exposure with DSCR loans. If a property underperforms or faces temporary vacancies, the investor’s personal finances are less at risk since the loan is primarily secured by the property’s income.

- Multiple Property Ownership: Investors with multiple mortgaged rental properties can use DSCR loans to streamline the financing process. These loans allow investors to consolidate the income and expenses from multiple properties to qualify for a single loan or to secure financing for additional properties.

- Scalability: DSCR loans are highly scalable, making it possible for investors to acquire a diverse range of properties, from single-family homes to large multifamily complexes or commercial properties, with the same financing approach.

- Cash Flow Management: DSCR loans encourage investors to focus on the cash flow potential of a property, helping them make informed investment decisions. Investors can assess whether a property’s rental income is sufficient to cover all associated expenses and generate a profit.

- Flexibility: DSCR loans offer flexibility in terms of property types. They can be used for a variety of real estate investments, including residential and commercial properties, as long as the property’s income meets the lender’s DSCR requirements.

- Entrepreneurship and Investment Growth: DSCR loans support entrepreneurial real estate investors who want to build a substantial and diversified real estate investment portfolio. This can create opportunities for wealth building and passive income generation.

Chapter 4: Examples of DSCR Loan Calculations

Here are four examples of Debt-Service Coverage Ratio (DSCR) calculations for different scenarios:

DSCR Below 1.00 (Not Favorable):

- Monthly Rental Income: $3,000

- Monthly Debt Service (Mortgage, Taxes, Insurance, Association Dues): $3,500

- DSCR = $3,000 / $3,500 = 0.857

In this example, the DSCR is below 1.00 (0.857), indicating that the property’s income falls short of covering its monthly debt service, which may raise concerns for lenders and investors.

DSCR At 1.00 (Break-Even):

- Monthly Rental Income: $4,000

- Monthly Debt Service: $4,000

- DSCR = $4,000 / $4,000 = 1.000

A DSCR of exactly 1.00 means that the rental income precisely matches the monthly debt service, indicating that the property breaks even, with no surplus or shortfall in covering expenses.

DSCR Above 1.20 (Favorable):

- Monthly Rental Income: $6,000

- Monthly Debt Service: $4,500

- DSCR = $6,000 / $4,500 = 1.333

Here, the DSCR is above 1.20 (1.333), suggesting that the property generates 33.3% more income than is needed to cover its debt service. This is considered a favorable and financially secure situation.

DSCR Above 1.50 (Very Favorable):

- Monthly Rental Income: $9,000

- Monthly Debt Service: $5,000

- DSCR = $9,000 / $5,000 = 1.800

A DSCR above 1.50 is considered very favorable.

In this scenario, the property generates 80% more income than required to cover its debt service, indicating a strong financial position and potential for surplus income.

These examples illustrate how the DSCR ratio can vary based on the property’s rental income and debt service expenses.

A DSCR above 1.00 indicates that the property is generating sufficient income to cover its expenses, with ratios above 1.20 and 1.50 being increasingly favorable and indicating a higher margin of safety for investors and lenders.

Conversely, a DSCR below 1.00 suggests that the property’s income falls short of covering its financial obligations, which may raise concerns about its financial viability.

Chapter 5: What Types of Properties Can Investors Use for DSCR Loans?

Debt-Service Coverage Ratio (DSCR) loans have various use cases across the real estate and investment landscape.

Here are some examples of DSCR loan use cases:

- Purchase of Rental Properties: DSCR loans are commonly used by real estate investors to purchase rental properties. Investors can use the rental income from the property being acquired to qualify for the loan, making it easier to expand their real estate portfolios.

- Refinancing Existing Mortgages: Investors with multiple rental properties may use DSCR loans to refinance existing mortgages on their properties. By doing so, they can potentially secure better terms and lower interest rates, improving cash flow.

- Multi-Unit Apartments: Investors looking to acquire or refinance multi-unit apartment complexes often turn to DSCR loans. The rental income from multiple units can be used to qualify for the loan.

- Commercial Real Estate: DSCR loans are suitable for financing various types of commercial properties, such as office buildings, retail spaces, industrial properties, and warehouses. Investors can use the rental income generated by these properties to secure financing.

- Vacation Rentals: Owners of vacation rental properties can use DSCR loans to finance their investments. Lenders assess the property’s income potential to determine loan eligibility and terms.

- Student Housing: DSCR loans are applicable to properties designed for student housing. Investors can use the rental income from student tenants to qualify for loans.

- Mixed-Use Properties: Properties combining residential and commercial spaces can qualify for DSCR loans if the rental income from both components supports the loan requirements.

- Assisted Living Facilities: DSCR loans may be used to finance senior housing, assisted living facilities, and nursing homes, provided that the rental income covers the debt service.

- Mobile Home Parks: Owners of mobile home parks can use DSCR loans to finance property acquisition or improvement projects when rental income is the primary source of repayment.

- Scaling Real Estate Portfolios: Real estate investors seeking to rapidly expand their portfolios may utilize DSCR loans to acquire multiple properties simultaneously, leveraging the rental income from existing assets.

- Self-Employed Investors: DSCR loans are advantageous for self-employed investors who may have irregular income or difficulty demonstrating traditional sources of income.

- Fix-and-Hold Strategy: Investors looking to renovate properties and convert them into income-generating assets can use DSCR loans during the acquisition phase and then refinance once the property is stabilized.

These examples showcase the versatility of DSCR loans in the real estate investment world.

They allow investors to leverage the income potential of their properties, manage cash flow effectively, and pursue various investment strategies and property types.

Chapter 6: How Do I Increase the DSCR Ratio?

Increasing the Debt-Service Coverage Ratio (DSCR) is essential for ensuring the financial health and stability of a real estate investment.

A higher DSCR indicates a greater margin of safety and improved ability to cover debt obligations.

Here are several strategies to increase your DSCR ratio.

Increase Rental Income:

- Raise Rent: If the current rental rates are below market value, consider increasing them gradually to boost rental income.

- Lease Additional Units: Fill any vacant units or rent out any unused spaces within the property to generate additional income.

Decrease Operating Expenses:

- Control Costs: Implement cost-effective property management practices to reduce expenses, such as maintenance, utilities, and property management fees.

- Review Contracts: Periodically review contracts with service providers to ensure you are getting competitive rates.

Refinance at Lower Interest Rates:

- Explore Refinancing: If interest rates have decreased since your initial financing, consider refinancing the loan to reduce monthly interest expenses.

Extend Loan Terms:

- Negotiate Loan Terms: Extending the loan term can lower monthly principal and interest payments, which may improve the DSCR. Discuss this option with your lender.

Increase Property Occupancy:

- Reduce Vacancies: Minimize property vacancies by improving marketing strategies and tenant retention efforts.

Add Income Streams:

- Offer Amenities: If feasible, provide additional income-generating amenities or services within the property, such as laundry facilities, vending machines, or parking spaces.

Implement Efficiency Upgrades:

- Make Energy-Efficient Improvements: Invest in energy-efficient upgrades (e.g., LED lighting, insulation, HVAC improvements) to lower utility costs and increase property value.

Adjust Property Management:

- Self-Manage: Consider self-managing the property to reduce property management fees, but ensure you have the time and expertise to do so effectively.

Diversify Your Portfolio:

- Invest in Higher-Income Properties: Acquire properties with higher rental income potential to increase overall cash flow and DSCR across your portfolio.

Set Aside Reserves:

- Establish Cash Reserves: Create a reserve fund to cover unexpected expenses, ensuring that the property can continue to meet its debt service even during challenging times.

Increase Property Value:

- Property Appreciation: Over time, property appreciation can increase its value, allowing you to potentially refinance or sell at a profit, which can positively impact the DSCR.

Reduce Debt Obligations:

- Pay Down Debt: If feasible, make extra principal payments to reduce the outstanding loan balance, which will lower future interest payments and improve the DSCR.

Improve Tenant Screening:

- Select High-Quality Tenants: Conduct thorough tenant screening to reduce the risk of rental defaults and vacancies.

Monitor and Adjust:

- Continuously Monitor: Regularly review the property’s financial performance and make adjustments as needed to maintain a healthy DSCR.

It’s important to note that increasing the DSCR may require a combination of these strategies, and the feasibility of each option can vary depending on the specific property, market conditions, and your investment goals.

Chapter 7: What are Some Problems Lenders May Have with DSCR Loans?

When dealing with Debt Service Coverage Ratio (DSCR) and loans, there can be several surprises that borrowers may encounter, which can impact their ability to secure a loan or manage their existing debt.

Lenders may have issues with the following:

- Unexpected DSCR requirements: Lenders may have stricter DSCR requirements than anticipated. Borrowers may be surprised to find that they need a higher DSCR to qualify for a loan, making it more challenging to secure financing.

- Fluctuating income: If a borrower’s income fluctuates significantly due to seasonal or irregular earnings, it can be challenging to maintain a stable DSCR. Lenders may be surprised by these income variations and may request additional documentation or higher DSCR thresholds to compensate.

- Interest rate adjustments: For variable-rate loans, borrowers may be surprised by interest rate adjustments, which can impact their DSCR by increasing debt service costs. Rising interest rates can make it more difficult to maintain a healthy DSCR.

- Balloon payments: Some loans have balloon payments, where a significant portion of the principal is due at the end of the loan term. Borrowers may be surprised by the size of the balloon payment, which can strain their DSCR and financial stability when it comes due.

- DSCR covenants: Lenders may include DSCR maintenance covenants in loan agreements, requiring borrowers to maintain a specific DSCR throughout the loan term. Borrowers who struggle to meet these requirements may face penalties or even default.

- Unexpected expenses: Unforeseen expenses or emergencies can reduce a borrower’s cash flow and impact their ability to maintain a healthy DSCR. These expenses can come as a surprise and put pressure on debt service.

- Declining property or asset value: If the value of the property or asset securing the loan decreases significantly, it can lead to a lower DSCR. Borrowers may be surprised by the impact of declining property values on their ability to meet debt obligations.

- Tenant vacancies: For real estate investors, unexpected tenant vacancies can disrupt rental income and negatively affect the DSCR. A sudden drop in occupancy can catch borrowers off guard.

- Economic downturns: A recession or economic downturn can impact a borrower’s income and business performance, making it challenging to maintain a healthy DSCR. Economic surprises can significantly affect loan repayment capacity.

- Inaccurate financial projections: If borrowers rely on inaccurate or overly optimistic financial projections when applying for a loan, they may be surprised when the actual financial performance falls short, leading to a weaker DSCR.

To avoid these surprises, borrowers should conduct thorough financial planning and analysis, regularly monitor their DSCR, maintain a financial cushion for unexpected expenses, and have contingency plans in place for adverse economic conditions.

It’s also essential to communicate openly with lenders and seek their guidance if facing challenges in meeting DSCR requirements or managing debt.

Chapter 8: When is a DSCR Loan Not a Good Idea?

A Debt Service Coverage Ratio (DSCR) loan may not be a good fit for certain borrowers or specific financial situations. Here are some scenarios in which a DSCR loan may not be suitable:

- Insufficient cash flow: If a borrower’s cash flow is consistently insufficient to cover their debt service obligations, a DSCR loan may not be the right choice. It’s crucial to have a comfortable margin of safety in your DSCR to ensure you can meet your debt payments without stress.

- Start-up businesses: Start-up companies often have uncertain or limited cash flow in the early stages. Lenders may be hesitant to offer DSCR loans to such businesses because of the higher risk of default. In these cases, other types of financing, like equity investments or business credit lines, might be more appropriate.

- Negative DSCR: A negative DSCR means that your cash flow is insufficient to cover your debt payments, indicating financial distress. Borrowers in this situation should consider debt restructuring, refinancing, or seeking financial advice before taking on additional debt through a DSCR loan.

- Highly speculative investments: If you plan to use the loan proceeds for highly speculative ventures or investments with uncertain returns, lenders may be reluctant to approve a DSCR loan. They prefer to see a reasonable level of predictability and stability in your cash flow.

- Short-term financing needs: DSCR loans are typically used for longer-term financing, such as mortgages for real estate investments. If you need short-term capital or working capital for day-to-day operations, other financing options like lines of credit or trade credit may be more suitable.

- Unproven business model: Lenders may be wary of providing DSCR loans to borrowers with unproven or untested business models. They prefer to see a history of stable income and financial performance before extending such loans.

- High-risk industries: Certain industries, such as speculative real estate development or highly cyclical sectors, may carry higher inherent risks. Lenders may be cautious about offering DSCR loans to borrowers in these industries.

- Unwillingness to provide collateral: DSCR loans, especially in real estate, often require collateral to secure the loan. If you’re not comfortable or unable to provide the necessary collateral, a DSCR loan may not be a viable option.

- Inability to meet lender requirements: Lenders have specific DSCR thresholds and eligibility criteria. If you cannot meet these requirements due to your financial situation or business model, it may be challenging to secure a DSCR loan.

In situations where a DSCR loan is not a good fit, borrowers should explore alternative financing options, seek financial advice, and work on improving their financial position before considering additional debt.

It’s essential to choose the right financing solution that aligns with your financial goals and capacity to manage debt responsibly.

Chapter 9: What are the DSCR Loan Requirements?

Debt Service Coverage Ratio (DSCR) loan requirements can vary depending on the lender, the type of loan, and the specific circumstances of the borrower.

However, there are some common DSCR loan requirements that lenders typically look for:

- DSCR Threshold: Lenders often specify a minimum DSCR requirement that borrowers must meet to qualify for the loan. This threshold is typically expressed as a ratio, such as 1.25:1 or 1.50:1, indicating that the cash flow generated by the property or business must be at least 1.25 or 1.50 times greater than the debt service (principal and interest payments).

- Historical Cash Flow: Lenders may require borrowers to provide historical financial statements (typically the last two to three years) to demonstrate the property or business’s ability to generate sufficient cash flow to cover debt obligations.

- Future Projections: Borrowers may need to provide financial projections or a business plan showing that they can maintain the required DSCR throughout the loan term. These projections should be realistic and based on reasonable assumptions.

- Property or Business Appraisal: For real estate related DSCR loans, lenders often require a professional appraisal of the property to determine its current market value and ensure it provides adequate collateral for the loan.

- Creditworthiness: Lenders evaluate the creditworthiness of borrowers, including their credit scores, financial history, and overall financial stability. A strong credit profile can improve the chances of loan approval.

- Loan-to-Value (LTV) Ratio: In real estate lending, lenders may also consider the loan-to-value ratio, which compares the loan amount to the property’s appraised value. A lower LTV ratio can reduce risk for the lender.

- Debt Obligations: Lenders assess the borrower’s existing debt obligations, including outstanding loans and credit lines. They want to ensure that the borrower has the capacity to take on additional debt without becoming overleveraged.

- Loan Term: The length of the loan term can affect DSCR requirements. Longer-term loans may have lower DSCR thresholds compared to shorter-term loans.

- Interest Rate: The interest rate on the loan can impact the DSCR, as higher interest rates increase the debt service costs. Borrowers should be prepared for possible interest rate fluctuations during the loan term.

- Documentation: Borrowers are typically required to provide detailed financial documentation, including tax returns, bank statements, income statements, balance sheets, and other relevant financial records.

- Property or Business Type: The type of property or business being financed can influence the DSCR loan requirements. Some property types may have stricter DSCR criteria due to their perceived risk levels.

- Guarantees: Lenders may require personal or corporate guarantees, especially for commercial loans. These guarantees add an extra layer of assurance that the debt will be repaid.

It’s essential for borrowers to carefully review the specific DSCR loan requirements provided by their lender and ensure they meet all the criteria before applying for the loan.

Additionally, borrowers should consider working with financial advisors or consultants to prepare a strong loan application and meet the lender’s expectations.

Chapter 10: How to Select a DSCR Lender (The Vetting Process)

When seeking a Debt Service Coverage Ratio (DSCR) loan, it’s crucial to choose the right lender to ensure that your financing needs align with the lender’s terms and requirements.

Here are some key factors to look for when selecting a DSCR lender:

- Experience and Specialization: Look for lenders with experience in providing DSCR loans, especially in your specific industry or property type. Lenders who specialize in your area of interest are more likely to understand your unique financing needs.

- DSCR Requirements: Different lenders may have varying DSCR requirements. Evaluate whether the lender’s DSCR threshold aligns with your financial situation and the property or business you intend to finance.

- Loan Terms: Consider the loan term and structure offered by the lender. Determine if the loan’s duration suits your needs and inquire about any flexibility in repayment options.

- Interest Rates: Compare interest rates offered by different lenders. Low-interest rates can significantly impact your ability to maintain a healthy DSCR. Be sure to understand whether the rates are fixed or variable.

- Fees and Costs: Inquire about any origination fees, closing costs, or ongoing servicing fees associated with the loan. Understanding these costs upfront is essential for evaluating the overall affordability of the loan.

- Loan-to-Value (LTV) Ratio: For real estate loans, the LTV ratio can affect the amount of financing you can secure. Find out the lender’s LTV requirements and whether they align with your property’s appraised value.

- Approval Process: Understand the lender’s approval process, including the timeline for loan approval and disbursement. Some lenders may offer expedited processes for borrowers in urgent need of financing.

- Customer Service: Assess the lender’s reputation for customer service and responsiveness. A lender with a reputation for being attentive to borrower needs can make the loan process smoother.

- Flexibility: Consider whether the lender is willing to work with borrowers who have unique circumstances or financial challenges. Some lenders may be more flexible than others in structuring loans.

- Financial Stability: Evaluate the lender’s financial stability and reputation within the industry. You want a lender that can provide long-term support and stability for your financing needs.

- Additional Services: Some lenders offer additional services beyond loans, such as financial advice, credit counseling, or investment guidance. These services can be valuable for borrowers looking to improve their financial position.

- Terms and Conditions: Carefully review the loan agreement and its terms and conditions. Pay attention to any covenants, requirements, or clauses that may impact your ability to maintain a strong DSCR.

- References and Reviews: Seek references or read online reviews to gain insights into other borrowers’ experiences with the lender. Positive feedback from previous clients can provide confidence in your choice.

- Compliance and Regulatory Considerations: Ensure that the lender complies with all relevant regulatory requirements and follows ethical lending practices.

It’s advisable to obtain loan quotes and offers from multiple lenders and compare them based on these factors.

This allows you to make an informed decision that aligns with your financial goals and the specific requirements of your DSCR loan.

Chapter 11: District Lending Currently Offers DSCR Loans in 19 States

We have 20+ years of experience handling DSCR loans for real estate investors.

District Lending offers DSCR Loans in the following 19 states:

- Arizona

- California

- Colorado

- Florida

- Georgia

- Idaho

- Louisiana

- Maryland

- Michigan

- Minnesota

- New Jersey

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- South Carolina

- Tennessee

- Texas

- Washington

Why get a DSCR Loan with District Lending?

- Our team at District Lending will do the heavy lifting for you by shopping and comparing the nuisances of different lenders to fine tune the rate and experience.

- Insanely low documentation, no personal DTI calculations, no tax returns needed.

- Protection by using an LLC or other business entity.

- Real estate investors can get more than 10 mortgages with DSCR.

- Rent must at least cover the debt to be eligible.

Chapter 12: DSCR Loans Frequently Asked Questions (FAQs)

Here are some frequently asked questions (FAQs) about Debt Service Coverage Ratio (DSCR) loans:

What is a DSCR loan?

- A DSCR loan is a type of financing where the borrower’s ability to service their debt obligations is assessed using the Debt Service Coverage Ratio. It’s commonly used for real estate investments and business loans.

What is the Debt Service Coverage Ratio (DSCR)?

- The DSCR is a financial metric that compares a property or business’s net operating income (NOI) to its debt service (principal and interest payments). It indicates the property or business’s ability to generate sufficient cash flow to cover its debt obligations.

How is the DSCR calculated?

- The DSCR is calculated by dividing the property or business’s NOI by its total debt service (annual loan principal and interest payments). The formula is DSCR = NOI / Total Debt Service.

What is a good DSCR ratio?

- A DSCR ratio above 1.0 indicates that there is sufficient cash flow to cover debt payments. Lenders often require DSCR ratios above 1.25 or 1.50, depending on the type of loan and the lender’s criteria. A higher DSCR is generally considered better, as it provides a larger margin of safety.

What types of loans use DSCR analysis?

- DSCR analysis is commonly used for commercial real estate loans, including mortgages for apartment buildings, office spaces, and retail properties. It is also applied to business loans, particularly for companies with significant cash flow.

Can individuals apply for DSCR loans?

- Yes, individuals, investors, and businesses can apply for DSCR loans, but eligibility criteria and requirements may vary based on the lender and the purpose of the loan.

What factors can affect my DSCR?

- Several factors can impact your DSCR, including changes in rental income, operating expenses, interest rates, property vacancies, and the overall financial health of your business or investment.

Are DSCR loans riskier than traditional loans?

- DSCR loans can be riskier due to the emphasis on cash flow. If your cash flow decreases or becomes unstable, it can lead to a lower DSCR and increase the risk of default. However, if managed properly, DSCR loans can provide valuable financing options.

Are there alternatives to DSCR loans?

- Yes, alternatives to DSCR loans include traditional mortgage loans, personal loans, lines of credit, and equity financing. The choice depends on your specific financing needs and financial situation.

How can I improve my DSCR?

- To improve your DSCR, you can increase rental income, reduce expenses, refinance existing debt at lower rates, or consider additional revenue streams. Maintaining a healthy financial position is crucial.

What documents do I need to apply for a DSCR loan?

- Typically, you’ll need financial documents, such as income statements, balance sheets, tax returns, and a business plan or property information for real estate loans. Lenders may have specific documentation requirements.

Can I refinance a DSCR loan?

- Yes, it is possible to refinance a DSCR loan, especially if you can secure better terms, lower interest rates, or extended loan durations. Refinancing can help improve your cash flow and DSCR.

What types of properties are eligible for DSCR loans?

- DSCR loans can be used to finance various types of properties, including residential rental properties, commercial real estate, hotels, industrial facilities, and more.

Is personal credit history important for DSCR loans?

- Yes, personal credit history can be important, especially for individuals or small businesses seeking DSCR loans. Lenders may consider the borrower’s creditworthiness when making lending decisions.

Can I use projected income for DSCR calculations?

- Lenders may accept projected income for DSCR calculations, but these projections should be based on realistic assumptions and supported by a sound business plan.

What’s the difference between a DSCR loan and a traditional mortgage?

- DSCR loans focus on the property’s cash flow to determine eligibility, while traditional mortgages often rely more on the borrower’s credit score and personal income.

How does a DSCR loan impact my property’s equity?

- A DSCR loan can affect your property’s equity by increasing your debt obligations. As you repay the loan, your equity may gradually increase over time.

Can I use a DSCR loan to consolidate debt?

- Yes, DSCR loans can be used for debt consolidation, which may help improve your overall cash flow and DSCR by consolidating higher-interest debts into a single, lower-rate loan.

Are DSCR loans suitable for fix-and-flip real estate projects?

- DSCR loans are generally better suited for income-producing properties, but other financing options like hard money loans may be more appropriate for fix-and-flip projects.

Can I apply for a DSCR loan with a low DSCR ratio?

- While it may be more challenging, some lenders offer DSCR loans to borrowers with lower DSCR ratios, provided they meet other eligibility criteria and may require additional collateral or higher interest rates.

What is a Debt Yield Ratio (DYR), and how does it relate to DSCR?

- The Debt Yield Ratio (DYR) is another financial metric used in real estate financing. It measures the property’s annual net operating income as a percentage of the loan amount. DYR and DSCR are complementary ratios that lenders consider when evaluating loan risk.

Can I use DSCR loans for a new business venture?

- Yes, DSCR loans can be used for new business ventures, but lenders may require more robust financial projections and business plans to assess the risk associated with the venture.

What are the interest rates for DSCR loans?

- DSCR loan interest rates are typically 150 Basis Points (BPS) to 300 BPS more than traditional consumer loan interest rates. Why? Because they are higher risk loans for the lender.

Looking for a DSCR Loan at a Great Low Rate? WE CAN HELP!

You’ve got questions about DSCR loans.

We’ve got expert answers!

If you’re looking for a DSCR loan on an investment property, and want to close quickly and easily, you can get in touch with us HERE.

District Lending currently offers DSCR loans in the following states: Arizona, California, Colorado, Florida, Georgia, Idaho, Louisiana, Maryland, Michigan, Minnesota, New Jersey, Ohio, Oklahoma, Oregon, Pennsylvania, South Carolina, Tennessee, Texas, and Washington.

>> Click HERE to get a DSCR loan rate in 60 seconds or less!

About the Author

Brian Reese is a senior advisor and co-owner at District Lending. He is one of the world’s leading experts in veteran benefits, having helped millions of veterans secure their financial future since 2013. Brian is the founder VA Claims Insider, an education-based Coaching & Consulting company whose mission is to educate and empower veterans to get the VA disability benefits they’ve earned for their honorable service. A former active-duty air force officer, Brian deployed to Afghanistan in support of Operation Enduring Freedom. He is a distinguished graduate of management of the United States Air Force Academy and earned his MBA as a National Honor Scholar from the Spears School of Business at Oklahoma State University.

“As a military veteran, I’ve made it my life’s mission to help people live happier and wealthier lives. District Lending brings this mission to life. We believe in integrity, honesty, and transparency, which is why you’ll see our rates right on our website. You’ll find lower rates and zero lending fees, which means you can buy your dream home for less. The savings are passed on to you — the way it should be.”

– Brian Reese, Advisor and Co-Owner, District Lending