VA assumable loans are a unique financial tool available to both buyers and sellers.

Assuming a VA mortgage means a qualified buyer can take over the loan payments from the original borrower without needing to secure a new loan.

This guide will explain the intricacies of assumable VA loans, outlining their benefits, eligibility factors, risks and requirements, and the process to get one.

Table of Contents

What is a VA Assumable Loan?

A VA assumable loan is a mortgage originally issued to a veteran under the VA home loan program that can be transferred to a new buyer.

The major aspect of these loans is that the interest rate and remaining loan balance can be passed to the new borrower, potentially offering more favorable terms than a new mortgage in a rising interest rate environment.

With high interest rates in the United States, this is a huge benefit right now.

What are the Benefits of Assuming a VA Home Loan?

Here’s a list of 10 key benefits of assumable VA loans:

- Lower Interest Rates: VA loans often come with competitive interest rates, which can be advantageous for buyers assuming the loan, especially if current market rates are higher.

- No Down Payment: VA loans typically do not require a down payment, so assuming an existing VA loan means the buyer can purchase the property without having to make a significant upfront payment.

- No Private Mortgage Insurance (PMI): VA loans do not require PMI, which can save the buyer money on their monthly mortgage payments.

- Easier Qualification: VA loans have more lenient credit and qualification requirements compared to conventional loans, making it easier for buyers to assume the loan and qualify for financing.

- No Prepayment Penalties: VA loans do not have prepayment penalties, so the buyer can pay off the loan early without incurring additional fees.

- Preservation of VA Loan Entitlement: When a VA loan is assumed, the seller’s VA loan entitlement may be preserved, allowing them to potentially use their VA benefits for a future home purchase.

- Faster Closing Process: Assuming a VA loan can often result in a quicker closing process since the loan is already in place, and there may be fewer documentation and approval requirements compared to securing a new loan.

- Lower Closing Costs: Buyers may benefit from lower closing costs when assuming a VA loan because some fees associated with originating a new loan may be waived or reduced.

- Favorable Loan Terms: Buyers can inherit the existing loan terms, which may include fixed or adjustable interest rates and favorable loan conditions.

- Competitive Advantage for Sellers: Offering an assumable VA loan can make a property more attractive to potential buyers, potentially increasing the pool of interested parties and speeding up the selling process.

What are the Eligibility and Requirements for Assumable VA Loans?

Here are the key eligibility and requirements for assumable VA loans in 2024:

Buyer Eligibility:

- The buyer assuming the VA loan must be eligible for a VA home loan. This typically requires the buyer to be an active-duty service member, a veteran, a member of the National Guard or Reserves, or a qualified surviving spouse.

- The buyer must meet the VA’s credit and income requirements, which can vary depending on the lender’s standards and the loan’s terms.

- The assuming buyer should intend to use the property as their primary residence.

VA Approval:

- The VA and the lender must approve the assumption of the loan. The lender will evaluate the assuming buyer’s creditworthiness and financial stability.

- The assuming buyer may be required to pay a fee for the VA’s processing of the assumption, which can vary.

Assumption Agreement:

- Both the buyer and the seller must complete and sign a VA loan assumption agreement, which outlines the terms and conditions of the assumption.

- The seller may remain partially liable for the loan until the lender formally releases them from responsibility.

Existing Loan Terms:

- The buyer assumes the existing VA loan, which means they inherit the loan’s current interest rate, principal balance, and repayment terms. These terms cannot be changed during the assumption process.

Funding Fee:

- The buyer may be required to pay a VA funding fee as part of the assumption process, unless they are exempt due to a disability related to military service. You must have a VA rating of 10% or higher to be eligible for the funding fee waiver.

Verification of Income and Credit:

- The lender will verify the buyer’s income and creditworthiness to ensure they can afford the loan payments.

- The assuming buyer may need to provide documentation, such as pay stubs, tax returns, and bank statements, as part of the application process.

Property Appraisal:

- In some cases, the lender may require a new appraisal of the property to determine its current value. This is done to ensure that the property’s value is sufficient to support the loan amount being assumed.

Release of Liability:

- The seller may seek a release of liability from the lender, which means they will no longer be responsible for the loan in the event of default by the assuming buyer. This release of liability is not guaranteed and must be negotiated between the parties and approved by the lender.

The 10 Step Process of Assuming a VA Loan

Here is the 10 step process to get an assumable VA loan:

#1. Determine Basic Eligibility:

- Verify that the buyer meets the eligibility requirements for assuming a VA loan. The buyer must be eligible for a VA home loan and intend to use the property as their primary residence.

#2. Find a Property:

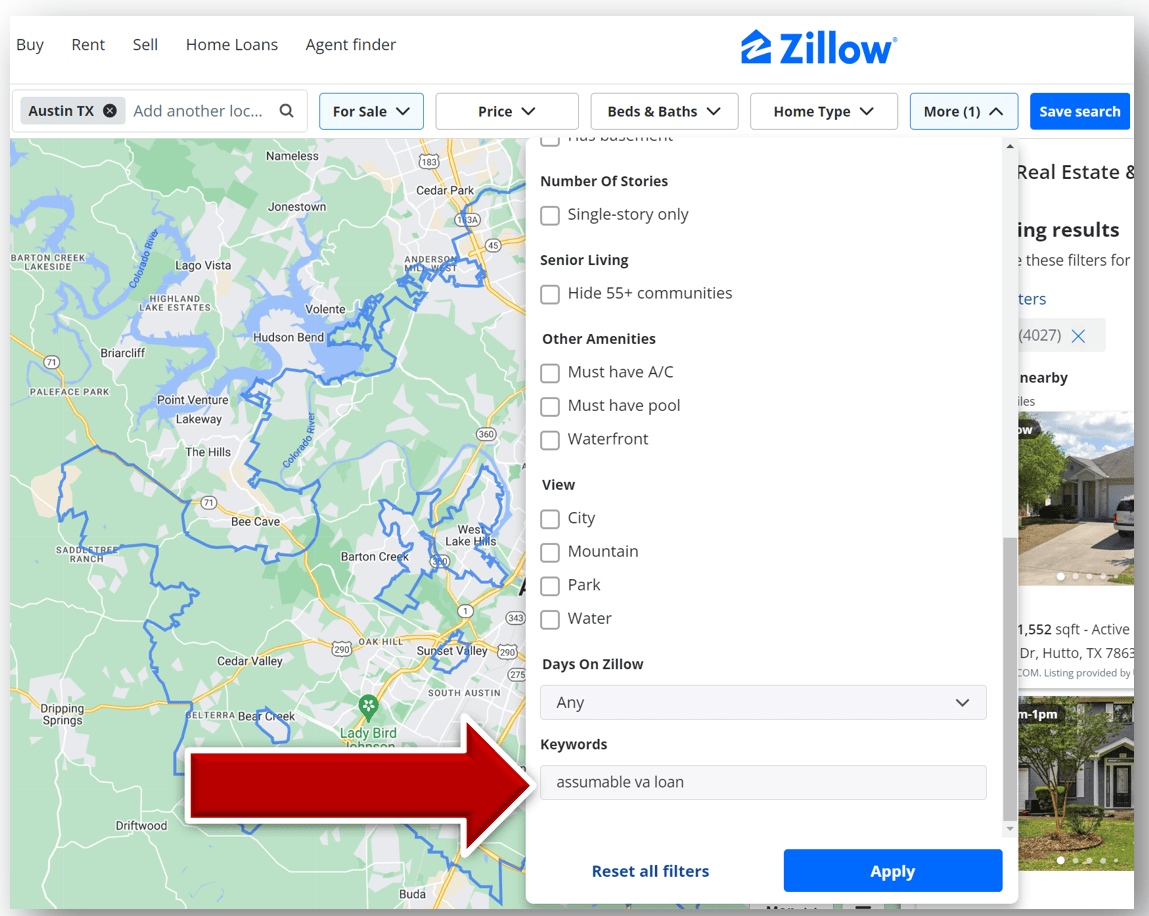

- The buyer and seller must agree on the terms of the sale, including the purchase price and other conditions. Zillow gives you a custom keyword entry option under the “More” menu button. You can also try including keywords related to loan types that you know are assumable, such as “VA loan,” “FHA loan,” or “USDA loan.”

#3. Obtain the Seller’s Approval:

- The seller must inform the lender of their intention to sell the property and have the loan assumed. The lender may require the seller to provide certain documentation and information.

#4. Obtain Lender Approval:

- The lender will review the assuming buyer’s financial qualifications, including their credit history and income, to determine if they are eligible to assume the loan.

- The lender may also request an updated appraisal of the property to assess its current market value. This is to ensure that the property’s value is sufficient to support the loan amount being assumed.

- If the buyer meets the lender’s criteria, the lender may issue a letter of approval for the assumption.

#5. Apply for VA Approval:

- The seller and buyer must complete a VA loan assumption application, which includes detailed information about the property, the buyer, and the seller.

- The VA will review the application and may charge a processing fee. Approval from the VA is necessary for the assumption to proceed.

#6. Negotiate Terms:

- The buyer and seller will negotiate the terms of the assumption, including the purchase price and any other conditions or concessions.

- The seller may request a release of liability from the lender, which would relieve them of any responsibility for the loan after the assumption.

#7. Sign Assumption Agreement:

- Both the buyer and the seller must sign an assumption agreement that outlines the terms and conditions of the assumption. This agreement will be provided by the lender.

#8. Closing:

- The closing process for an assumed VA loan is similar to that of a traditional home purchase. It involves signing all necessary documents, including the assumption agreement, and transferring ownership of the property.

- The buyer may be required to pay any applicable fees, such as the VA funding fee and closing costs.

#9. Inform the VA:

- After the closing, the lender will notify the VA of the completed assumption, and the VA will update its records to reflect the new owner.

#10. Start Making Payments:

- The assuming buyer is responsible for making monthly mortgage payments to the lender based on the terms of the assumed loan.

Risks and Considerations of Assumable VA Loans

While VA assumable loans offer benefits, there are risks and considerations for both buyers and sellers to be aware of.

For Buyers:

- Credit and Financial Qualifications: Assuming a VA loan still requires the buyer to meet the lender’s credit and financial requirements. If the assuming buyer’s financial situation doesn’t meet the lender’s standards, they may not be approved for the assumption.

- Interest Rate: The interest rate on the assumed VA loan is typically based on the original loan’s terms. If interest rates have increased since the original loan was taken out, the assuming buyer may miss out on lower rates available for new loans.

- Loan Balance: The buyer assumes the remaining balance of the existing VA loan. If the property’s current value is significantly lower than the loan balance, the buyer may need to make up the difference in cash or through other financing.

- VA Funding Fee: Depending on the circumstances, the buyer may be required to pay a VA funding fee as part of the assumption process. This fee can add to the overall cost of assuming the loan.

- Property Condition: It’s crucial for the buyer to conduct a thorough inspection of the property to assess its condition and any potential issues. The seller’s existing loan does not cover repairs or improvements to the property.

For Sellers:

- Release of Liability: While the seller is selling the property and transferring the loan to the buyer, they may remain partially liable for the loan until the lender formally releases them from responsibility. This means that if the assuming buyer defaults on the loan, it could impact the seller’s credit.

- Negotiating Terms: The seller and buyer must agree on the terms of the assumption, including the purchase price, any concessions, and whether the seller will request a release of liability. Negotiating these terms can be complex.

- Timing: The assumption process may take some time, and it’s essential for sellers to plan for a potentially extended closing timeline.

- Impact on VA Entitlement: The seller’s VA loan entitlement may be tied up with the assumed loan until the lender releases them from liability. This could affect the seller’s ability to use their VA benefits for another home purchase.

- Future Financing: Sellers should consider their future financing needs. If they plan to buy another home, they need to assess how the assumed loan and potential remaining liability may impact their ability to secure a new mortgage.

- Due-on-Sale Clause: Some VA loans may have a due-on-sale clause that allows the lender to demand the full loan balance upon transfer of the property. While this is rare with VA loans, it’s essential to check the loan documents.

How Do I Find Assumable VA Loans?

The best way to find assumable loans is to do online research and check out websites like TakeList, which list assumable mortgage loans across the country.

Major websites like Zillow and Realtor have custom keyword search features to find properties with assumable mortgages.

Conclusion & Wrap-Up

VA assumable loans can be a valuable option for both buyers and sellers, offering potentially lower interest rates and simplified loan processes.

However, understanding the eligibility requirements, process, and potential impacts on VA loan entitlement is crucial.

Both parties should consult with a mortgage professional to navigate the specifics of assuming a VA loan.

Need a Lender for Your VA Assumable Loan? WE CAN HELP!

You’ve got questions about an assumable VA loan.

We’ve got expert answers!

If you want to buy or refinance your home for less with a VA loan, you can get in touch with us HERE.

>> Click HERE to get a great low VA loan rate in 60 seconds or less!

About the Author

Brian Reese is a senior advisor and co-owner at District Lending. He is one of the world’s leading experts in veteran benefits, having helped millions of veterans secure their financial future since 2013. Brian is the founder VA Claims Insider, an education-based Coaching & Consulting company whose mission is to educate and empower veterans to get the VA disability benefits they’ve earned for their honorable service. A former active-duty air force officer, Brian deployed to Afghanistan in support of Operation Enduring Freedom. He is a distinguished graduate of management of the United States Air Force Academy and earned his MBA as a National Honor Scholar from the Spears School of Business at Oklahoma State University.

In Brian’s Words:

“As a military veteran, I’ve made it my life’s mission to help people live happier and wealthier lives. District Lending brings this mission to life. We believe in integrity, honesty, and transparency, which is why you’ll see our rates right on our website. You’ll find lower rates and zero lending fees, which means you can buy your dream home for less. The savings are passed on to you — the way it should be.”

– Brian Reese, Advisor and Co-Owner, District Lending