To qualify for VA home loan eligibility, you or your surviving spouse must meet the minimum military service criteria established by the VA.

Additionally, you must get a copy of your Certificate of Eligibility (COE) and meet the credit and income prerequisites set by your lender.

Okay, let’s explore how to qualify for a VA loan in more detail.

Table of Contents

Who Qualifies for VA Home Loan Eligibility?

There are 4 primary ways to qualify for VA home loan benefits based on your military service status.

You qualify for VA loan benefits if you meet one or more of the following minimum service requirements:

- You served 90 consecutive days of active service during wartime

- You served 181 days of active service during peacetime

- You have 6 years of service in the National Guard or Reserves or served 90 days (at least 30 of them consecutively) under Title 32 orders

- You are the spouse of a service member who died while serving or due to a service-related disability

What If I Don’t Meet the Minimum Service Requirements for a VA Loan?

Even if you don’t meet the minimum service requirements to get a VA loan, you may still be able to get a COE if you were discharged for one of the following reasons:

- Hardship, or

- The convenience of the government (you must have served at least 20 months of a 2-year enlistment), or

- Early out (you must have served 21 months of a 2-year enlistment), or

- Reduction in force, or

- Certain medical conditions, or

- A service-connected disability (a disability related to your military service)

How Do I Verify My VA Loan Eligibility Status?

Lenders require a VA Certificate of Eligibility (COE) to verify a Veteran’s compliance with the minimum service requirements.

By providing your social security number and date of birth, your lender can easily retrieve the necessary information.

While there are instances where the process may be more intricate, it’s important to note that you do not need the COE before applying for a VA loan.

Here are the three most common ways to get a copy of your VA COE:

- Applying through a VA-approved lender

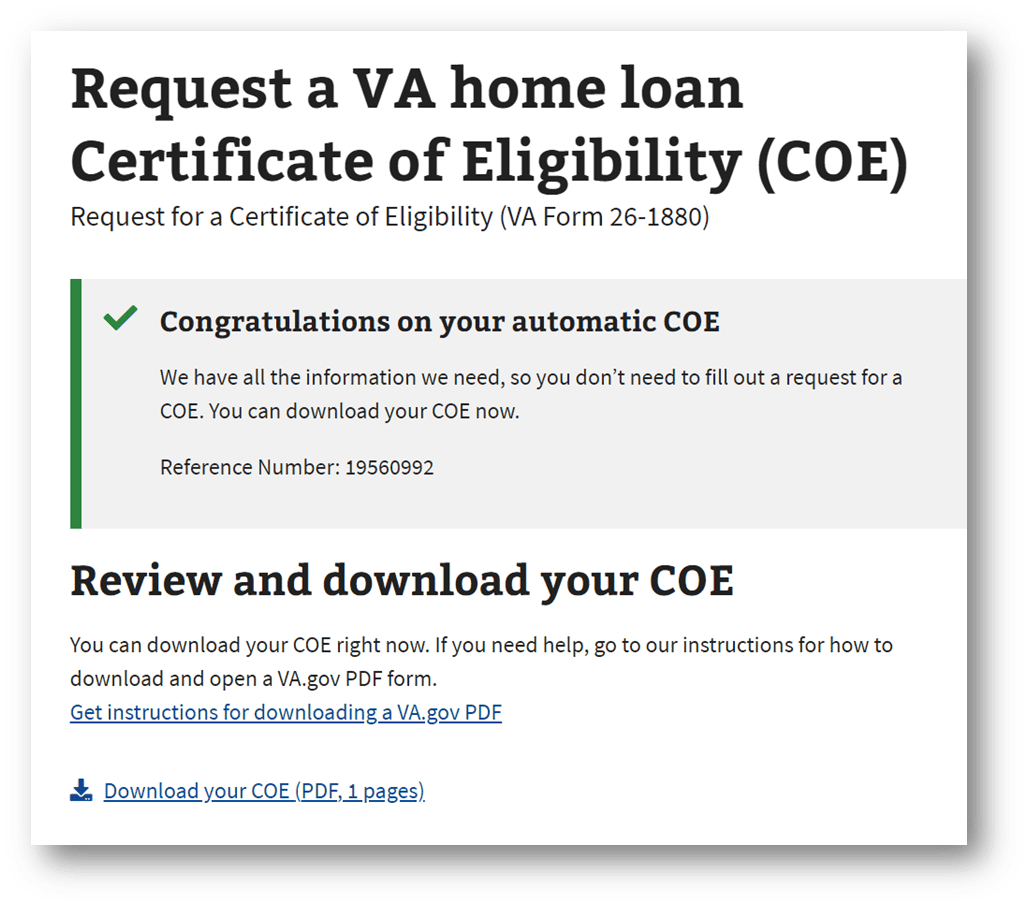

- Applying online at VA.gov HERE (takes about 30 seconds to download your COE)

- Applying by mail using the VA Form 26-1880

It’s super easy to get your VA Certificate of Eligibility (COE) online; it took me about 30 seconds to get mine online on the new VA.gov website.

What Documents Will My VA Home Loan Lender Need?

| Military Service Status | Documents Required |

| Veteran | DD 214 |

| Current or Former Activated National Guard or Reserves | DD 214 |

| Active Duty Military | Statement of Service |

| Current National Guard or Reserves (Never Activated) | Statement of Service and an allocated points statement |

| Discharged National Guard (Never Activated) | NGB Form 22 (Report of Separation and Record of Service) and NGB Form 23 (Retirement Points Accounting and proof of the character of service) |

| Discharged Reserves (Never Activated) | Army Reserve: DARP Form FM 249-2E or ARPC Form 606-E. Navy Reserve: NRPC 1070-124. Air Force Reserve: AF 526. Marine Corps Reserve: NAVMC HQ509 or NAVMC 798. Coast Guard Reserve: CG 4174 or 4175 |

How Can a Surviving Spouse Verify Eligibility for a VA Loan?

Surviving spouses who wish to utilize their VA loan benefits must also possess a Certificate of Eligibility (COE) to confirm their eligibility.

The process of obtaining a COE as a surviving spouse depends on whether you are receiving Dependency and Indemnity Compensation (DIC).

If you are receiving DIC benefits, you will need to complete VA Form 26-1817 (Request for Determination of Loan Guaranty Eligibility – Unmarried Surviving Spouses) and acquire a copy of the Veteran’s separation documents, such as a DD Form 214.

On the other hand, if you are not receiving Dependency and Indemnity Compensation benefits, you will need to apply using VA Form 21P-534EZ and submit it to your state’s VA Pension Management Center.

In addition, you will be required to provide a copy of your marriage license, the Veteran’s death certificate (or DD Form 1300 – Report of Casualty), and the Veteran’s separation paperwork.

Can I Talk to the VA About Home Loan Eligibility Status?

Yes, you can talk to VA representatives about your basic eligibility for a VA home loan.

If you have any questions, please call your VA regional loan center 1-877-827-3702.

Representatives are available Monday through Friday, 8:00am to 6:00pm eastern time.

Want to Use Your VA Home Loan Benefits?

You’ve got VA loan questions.

We’ve got expert answers!

If you’re thinking about a purchase or refinance mortgage using your VA home loan benefits, or if you have questions about getting the best interest rate, obtaining jumbo loan financing, or any other questions about what loan products you may qualify for, you can get in touch with us HERE.

>> Click HERE to get a great low mortgage rate in 60 seconds or less!

About the Author

Brian Reese is a senior advisor and co-owner at District Lending. He is one of the world’s leading experts in veteran benefits, having helped millions of veterans secure their financial future since 2013. Brian is the founder VA Claims Insider, an education-based Coaching & Consulting company whose mission is to educate and empower veterans to get the VA disability benefits they’ve earned for their honorable service. A former active-duty air force officer, Brian deployed to Afghanistan in support of Operation Enduring Freedom. He is a distinguished graduate of management of the United States Air Force Academy and earned his MBA as a National Honor Scholar from the Spears School of Business at Oklahoma State University.

In Brian’s Own Words:

“As a military veteran, I’ve made it my life’s mission to help people live happier and wealthier lives. District Lending brings this mission to life. We believe in integrity, honesty, and transparency, which is why you’ll see our rates right on our website. You’ll find lower rates and zero lending fees, which means you can buy your dream home for less. The savings are passed on to you — the way it should be.”

– Brian Reese, Advisor and Co-Owner, District Lending